RECURSOS PARA EL CONSUMIDOR

Recursos para la compra o venta de una vivienda, impuestos sobre la propiedad y más.

¿ESTÁS PENSANDO EN COMPRAR UNA CASA POR TU CUENTA?

Aquí está tu lista de tareas

Get Informed - Do Your Research

- Research the real estate industry and legal services to understand what’s available to you, including the entire process and necessity for legal representation.

- Achieve proficiency in federal and state fair housing laws that protect your rights. You want to be sure that you’re not being denied the opportunity to make an offer on a home or secure financing based on your race, religion, national origin, sex, disability, and/or family status.

- Research local and national down payment assistance resources. These programs can help make your home purchase more affordable.

- Check your eligibility for down payment assistance programs.

- If you’re a Veteran, research home services and loan programs available to you.

- If you’re a Veteran, determine whether you qualify for a zero-down VA home loan. Making a down payment is a significant hurdle for many home buyers. Programs like these can open the door to homeownership, for those who know about them and qualify.

- Learn about local home prices, inventory levels, and market demand in your desired area. If you are in a hotter market, high demand for homes may affect your buying process and offer strategy.

- Ensure that all personal and financial information remains confidential to mitigate risk of identity theft. Research the steps that you can take to protect your identity when buying a home.

- Throughout the process, know the risks of posting home search details on social media to avoid being targeted for fraud.

- Do some research on what home features are currently popular to help identify your preferences and how this may affect the value of the home.

Set Homeownership Goals and Budget

- Obtain a copy of your credit report, including your credit score, to assess where you stand, and ensure you have time to dispute errors and improve your score. The better your credit score, the more likely you are to be approved for a mortgage and receive a better rate.

- Consider all your homeownership wants and non-negotiable needs. You may need a certain number of bedrooms based on the size of your family, or a first-floor bedroom and bathroom if you plan to age in place.

- Set your budget and be mindful of the complete cost of homeownership. Consider the purchase cost of the home and any ongoing living and maintenance expenses. Those ongoing expenses may include but are not limited to real estate taxes, heating, AC, water, yard and appliance maintenance, repairs, homeowners association fees, and commuting costs.

- Assess your financial ability to purchase a home. The typical rule of thumb is that your total monthly housing payment (mortgage, taxes, insurance, etc.) shouldn’t be more than 30% of your gross monthly household income, but individual situations may vary.

- Assess your desired market’s compatibility with your budget based on current income and other considerations.

- Professionally advocate for yourself throughout the entire process. To do that, you should promote and defend your interests while keeping emotions in check to ensure you get your desired outcome.

Start Your Home Search

- Establish and adhere to a schedule for house hunting, mortgage approval, and closing to meet your desired timeline. If you miss any milestone deadlines, you could be at risk of losing your down payment or losing the home for purchase.

- Learn how local markets could affect your buying and owning process. Fewer homes for sale, future development plans, school ratings, access to transportation, and community amenities are all elements that may affect demand in a given market.

- Scout listings and online marketplaces for suitable properties.

- Set up real-time alerts on home search marketplaces to get notifications when matching homes hit the market, and for open houses and price reductions.

- Compare properties to your wants and needs list to ensure they align with what you’re looking for.

- Tap your personal network to uncover additional properties of interest that are not yet publicly listed and may become available for sale soon.

- Contact homeowners in desired areas to see if they are considering selling.

- Gather information about any homes that might be for sale but are not actively being marketed.

- Virtually preview properties that you’re interested in.

- Select homes for viewing that align with your specific needs.

- Schedule multiple in-person home viewings by contacting each home’s listing agent. Schedule separate appointments at times that suit the listing agent but may not always suit you.

- Periodically reevaluate your needs and refocus your property search, as necessary.

- Explore all available resources to learn more about prospective neighborhoods. Be sure to speak to local experts who understand the neighborhood and will give you honest feedback.

- Tour the amenities, schools, and points of interest, and test commute times in your chosen search area.

- Cross-reference local crime registries for the neighborhoods you are searching.

- Educate yourself on what to look for in property disclosures of home listings while you search to make informed decisions. Required property disclosures vary by state and may include, but are not limited to rights of way, upcoming special assessments, whether the home is in a flood zone, past termite damage, and the presence of lead paint.

- Stay current with the listing months of market inventory. As with days on the market, this indicates how competitive a given market is and should inform your offer.

- Consider measures of home value beyond price per square foot. These include neighborhood, proximity to work and community amenities, and community development plans. Be sure to consult with a local expert to get the most comprehensive information.

- Research municipal services and other relevant neighborhood information.

- Be informed about potential neighborhood negatives such as noise levels, venues, or operations that could impact your property value.

- Check applicable zoning and building restrictions if you plan to rent out your home or add a unit to generate short-term or monthly rental income.

- Understand public property and tax information for potential homes. It’s important to be informed about the possibility of future tax increases and property assessments, which will affect the property taxes you owe from year to year.

- Gather and consider important data on utility availability and costs. For example, you’ll want to confirm if the home has good high-speed internet access.

- Research any environmental factors and risks that could affect your home, such as flooding, wildfire, heat, air quality, and noise. Some of these factors will affect the cost of ownership. For example, if the home you purchase is in a flood zone, you will need to obtain flood insurance.

- Narrow down your top home choices for a closer look before considering making any offer.

Prepare Financing

- Analyze your finances to determine the total down payment and closing costs you can afford.

- Gather and assess quality lender resources. Ask friends and family for recommendations.

- Consider at least three mortgage lenders during the pre-approval process. Mortgage rates, terms, and eligibility may vary from lender to lender.

- Familiarize yourself with the mortgage pre-approval process. Pre-approval means that a lender has verified your income, credit background, and other factors and has provided a conditional commitment for an approved mortgage amount. With pre-approval, your offer will be considered far more seriously.

- Prepare and collect personal financial information like pay stubs, credit card statements, and other existing loans/debt, and share that information with the lenders you’re considering.

- Collect and compare multiple financing options. Beyond traditional mortgages, look into lesser-known alternative options like seller financing or rent-to-own programs.

- Explore various financing options to find the best fit for your needs. Many people use a conventional, fixed-rate 30-year mortgage, but mortgages with other terms (e.g., 15- and 10-year fixed rate, adjustable rate, and assumable) might also be options.

- Coordinate with your lender to discuss discount points, which you can pay to lower the interest rate on your loan.

- Analyze loan estimates. Loan duration, size of your down payment, fees, and other loan terms can affect your overall mortgage costs.

- Obtain a pre-approval letter from your lender, which is more comprehensive than pre-qualification. Pre-approval is a written commitment from a lender that stipulates the amount they will lend you for a home purchase.

- Carefully review the pre-approval letter from your lender to understand its contents and ask necessary questions.

Making Your Offer

- Review statistics to see what percentage of the list price sellers in your area are currently receiving. Review recent sales to see how long homes like the one you want are staying on the market.

- Leverage available resources to negotiate with the seller. You’ll want to be sure that you’ve found all possible information about the home and are making a strong offer.

- Review available inspection data before making an offer. Inspections are your opportunity to uncover issues with the property that you may not have noticed during your home search.

- Submit a strong offer backed by market research to make sure you’re offering a competitive price.

- Consider adding a personalized letter to your offer. This could help set you apart and make your offer stand out from others.

- Include contingencies in your offer that protect you in case the deal falls through. Examples of contingencies are obtaining financing, selling your current home, satisfactory home inspection, and completing the sale by a certain date. You’ll want to work with your real estate professional to understand your options for contingencies and whether they will make your offer more or less appealing to the seller.

- Be sure to respond to counteroffers in a timely manner. Consider them carefully and strategically.

- Remain flexible in negotiations to increase your chances of a successful offer. For example, being open to closing on the seller’s timeline might make your offer more appealing.

- Stay informed throughout the negotiation process to ensure you understand the contract and meet all deadlines. For example, you’ll need to ensure you understand the terms of the contract, respond to counteroffers in a timely manner, and prepare to meet any contingencies you’ve set.

Closing the Deal

- Secure an inspection as soon as possible after signing the purchase agreement to reveal any potential issues with the property.

- Consider hiring a professional for the inspection. While a professional inspection may cost several hundred dollars, it can reveal hidden issues that may be costly to fix later.

- After the inspection, negotiate repairs or credits with the seller if necessary. You can ask the seller to make the repairs or ask for credits or price reductions to cover the costs of repairs.

- Final review and approval of your financing application with your lender.

- Work with your lender to complete the home appraisal to determine the value of the home. The lender will order the appraisal, which usually costs several hundred dollars. The appraisal must be completed before the lender can approve your loan.

- After the appraisal, work with your lender to finalize the terms of your mortgage. The lender will review the appraisal, verify your income, and complete any other necessary steps to finalize your mortgage.

- Coordinate with your real estate professional, lender, and title company to ensure all necessary paperwork is completed before the closing date. This will include the closing disclosure, which lists the final terms and costs of your mortgage.

- Conduct a final walk-through of the home to ensure it’s in the expected condition and any agreed-upon repairs have been made. This usually takes place a few days before the closing date.

- Review the closing disclosure carefully and ask questions about any terms or costs you don’t understand.

- Be sure to bring all necessary documents and funds to the closing meeting. This includes a valid ID, proof of homeowner’s insurance, and a cashier’s check or wire transfer for the down payment and closing costs.

- Sign all closing documents, including the mortgage note, deed of trust, and other necessary paperwork.

- Receive the keys to your new home and celebrate your successful purchase!

Actual services or to-dos will depend on the needs of the buyer and the transaction - not all 111 things will need to be done in every transaction. Information based on a 2023 proprietary survey among recent home buyers and sellers. Provided in partnership with realtor.com.

¿POR QUÉ CONTRATAR A UN AGENTE INMOBILIARIO?

Antes de adentrarte por tu cuenta en el mundo inmobiliario, considera la posibilidad de contactar con un agente inmobiliario. Aquí te explicamos por qué deberías hacerlo.

Los agentes inmobiliarios están sujetos a un estándar ético más elevado.

No todos los agentes inmobiliarios son REALTORS®. Los REALTORS® se comprometen a cumplir un Código de Ética que va más allá de lo exigido por la ley, priorizando sus intereses y estableciendo altos estándares de conducta profesional.

Lea el Código de Ética de REALTOR®

Si cree que un REALTOR® ha violado el Código de Ética, puede presentar una queja.

Los agentes inmobiliarios hacen mucho más que ayudarle a comprar y vender bienes raíces.

Protegen los derechos de los propietarios. Se oponen a las propuestas que aumentarían las cargas para comprar, vender y poseer bienes inmuebles. Y trasladan las inquietudes de los propietarios a la Legislatura, los organismos reguladores y las autoridades locales.

Obtenga más información sobre cómo los REALTORS® de Texas abogan por usted.

Los agentes inmobiliarios tienen acceso a educación y recursos especializados.

Además de los cientos de horas de clase necesarias para obtener una licencia de bienes raíces, los agentes inmobiliarios de Texas (Texas REALTORS®) aprovechan las oportunidades de formación continua para mantenerse al día sobre las tendencias y novedades del sector. Muchos agentes inmobiliarios de Texas también realizan formación especializada para ofrecer un mejor servicio a distintos grupos de consumidores, como lo demuestran las siglas que suelen acompañar a sus nombres (conocidas como designaciones o certificaciones).

A través de su asociación, los REALTORS® también tienen acceso exclusivo a más de 100 formularios relacionados con la actividad inmobiliaria, lo que facilita su transacción y le ahorra tiempo.

Los agentes inmobiliarios saben cómo fijar el precio de una vivienda con precisión.

Si bien puedes usar un sitio web de valoración de viviendas que te dé una cifra aproximada, no deberías basarte únicamente en ella. Estos sitios a menudo desconocen los detalles de tu propiedad, el mercado actual y lo que buscan los compradores en tu zona. Un agente inmobiliario puede ayudarte a determinar un precio más preciso para tu propiedad.

Los agentes inmobiliarios pueden acotar su búsqueda de vivienda.

Podrías pasar horas buscando propiedades en línea, contactando a propietarios o agentes para verlas y evaluando si es una buena inversión. O bien, podrías contratar a un agente inmobiliario para que te ayude a simplificar la búsqueda, identifique tus necesidades, encuentre propiedades que se ajusten a ellas y organice visitas. Además, te ayudará a determinar si el precio es adecuado y qué puedes pagar.

Los agentes inmobiliarios son negociadores expertos.

No todo el mundo tiene habilidades de negociación, pero los agentes inmobiliarios sí. Cuentan con la información más actualizada sobre leyes, el mercado y mucho más, lo que les permite negociar en su nombre con confianza.

Los agentes inmobiliarios gestionan el proceso y le ahorran tiempo.

Los agentes inmobiliarios pueden ahorrarle mucho tiempo y molestias al encargarse de las tareas que usted no tiene tiempo de gestionar. Por ejemplo, los agentes inmobiliarios tienen experiencia en la comercialización de propiedades, lo que significa que no tiene que elaborar un plan por su cuenta. Además, facilitan y explican todo el proceso de la transacción para que usted no tenga que estar pendiente de cada detalle.

GUÍAS PARA EL CONSUMIDOR

Las transacciones inmobiliarias pueden ser complicadas. Estas guías pueden ayudar.

Acuerdos escritos de compra

Al buscar una vivienda, se le pedirá que firme un contrato de compraventa por escrito después de haber elegido al profesional con el que desea trabajar.

Jornadas de puertas abiertas y acuerdos por escrito

Los profesionales inmobiliarios de todo el país solicitarán a los compradores que firmen un contrato por escrito antes de visitar una vivienda. ¿Pero qué ocurre si solo se va a una jornada de puertas abiertas?

Negociación de acuerdos de compraventa por escrito

Esto es lo que debes saber sobre cómo negociar un acuerdo de servicios y compensación con un agente que sea REALTOR®.

Ofertas de compensación

Esto es lo que debes saber sobre un vendedor o agente que ofrece compensar a otro agente por conseguir un comprador que cierre con éxito la transacción.

Acuerdos de listado

Una de las primeras cosas que harás al vender tu casa es negociar y firmar un contrato de venta con tu agente.

Servicios de listado múltiple

Al comprar o vender una casa, su agente puede usar un MLS para encontrar casas en venta o promocionar su propiedad. Esto es lo que necesita saber.

Concesiones del vendedor

Los vendedores de viviendas pueden optar por ofrecer concesiones para atraer compradores o cerrar un trato. Descubra si este enfoque es adecuado para usted.

Comprar tu primera casa

Estás listo para encontrar tu primera casa. Descubre por dónde empezar y qué recursos tienes a tu disposición al iniciar tu camino hacia la compra de una vivienda.

Hipotecas y financiación

Un agente inmobiliario miembro de REALTOR® puede ayudarle a conocer las opciones para encontrar un préstamo que le permita pagar su nueva casa a lo largo del tiempo.

10 preguntas que debes hacerle a un agente del comprador

Si estás listo para comprar una casa, debes sentirte con la libertad de encontrar y trabajar con el agente que mejor se adapte a tus necesidades.

10 preguntas que debes hacerle al agente del vendedor

Si estás listo para vender tu casa, debes sentirte con la libertad de encontrar y trabajar con el agente que mejor se adapte a tus necesidades.

Pasos entre la firma y el cierre

Una vez que firme el contrato de compraventa de su nueva vivienda, aún quedarán varios pasos por completar antes de poder finalizar —o “cerrar”— la transacción.

GUÍAS ADICIONALES

Preparación para la compra de una vivienda

Impuestos sobre la propiedad

Depósito en garantía y dinero de arras

¿Qué factores influyen en la fijación del precio de su vivienda?

Asociaciones de propietarios de viviendas

Cómo protegerse del fraude de títulos de propiedad

Mercado del comprador frente a mercado del vendedor

Lo que los veteranos deben saber

El proceso de evaluación

Vivienda justa

Daños por incendio y cobertura de la póliza

Navegando por múltiples ofertas

Superando las barreras para la propiedad de vivienda

Los agentes inmobiliarios anteponen los intereses de sus clientes a los suyos propios.

Inspecciones de viviendas

Seguro contra inundaciones

Divulgaciones del vendedor

Escrituras y títulos

Deducción fiscal por intereses hipotecarios

Relaciones de agencia y no agencia

Seguro de vivienda

Preparándose para vender su casa

Comercializando tu hogar

Comprar un terreno y construir una casa nueva

Planificación de su hogar y patrimonio

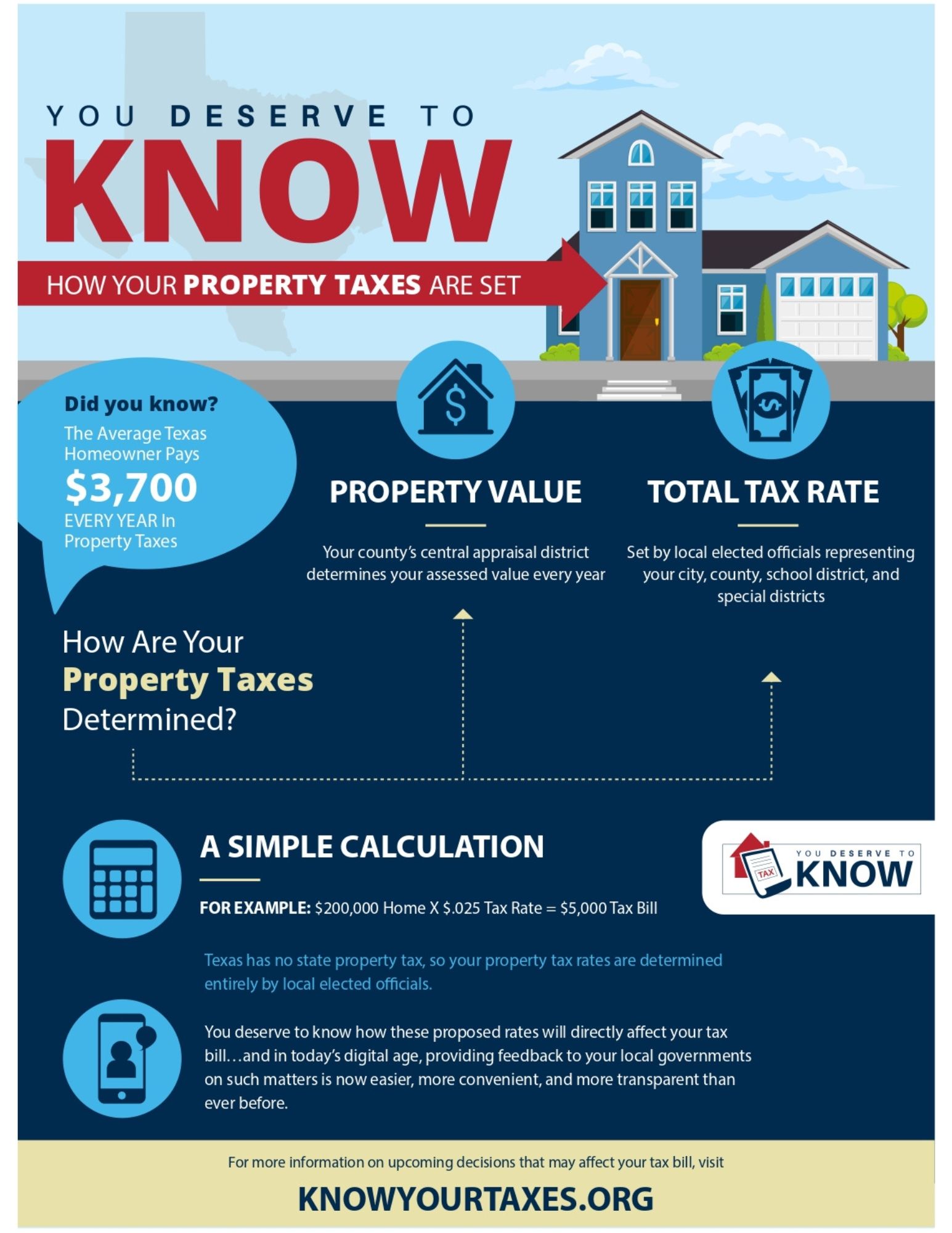

¿QUÉ SABES SOBRE

¿IMPUESTOS SOBRE LA PROPIEDAD?

Descubre quién tiene la potestad de determinar tu factura del impuesto predial, averigua qué es lo que...

Los números significan para su factura y acceso a muchos más recursos útiles.

KnowYourTaxes.org es un servicio proporcionado por Texas REALTORS®.

Finalidad de los impuestos sobre la propiedad

El dinero que usted recauda de sus impuestos sobre la propiedad se utiliza para financiar servicios comunitarios tales como:

- escuelas públicas

- proyectos de infraestructura

- Departamentos de policía y bomberos

- Y otros servicios locales

Los tipos impositivos que fijan anualmente los funcionarios locales electos de su distrito escolar, el tribunal de comisionados del condado y el ayuntamiento ayudan a determinar el importe de su factura de impuestos sobre la propiedad.

Exenciones de vivienda principal

El propietario de una vivienda tiene derecho a una exención de impuestos sobre la propiedad que constituye su residencia principal a partir del 1 de enero del año de tasación. Para obtener información sobre las exenciones, comuníquese con el distrito central de tasación de su condado.

ENLACES RÁPIDOS

Estadísticas de mercado

Consulte datos de mercado actuales e históricos hasta el nivel local. Nuestros informes incluyen gráficos y datos fáciles de comprender para ofrecerle rápidamente una visión general del mercado actual.